In recent times, we have seen a surge in e-payments, or what has now been termed cashless payments What is the cause of this gallop toward removing cash from some environments? Well, that is simple—cost savings, revenue generation and improved efficiencies.

The 2010 Football World Cup, in South Africa, and the 2014 basketball World Cup, in Spain, have plans for cashless facilities, and the 2009 German F1 Grand Prix, in Nurnberg, has already implemented a cashless solution. To demonstrate how increasingly important cashless technology has become to sports venues, Sandra Alzetta, Visa Europe‘s senior VP for consumer market development, said, “The aim is for a cashless Olympic Games in London in 2012.”

|

|

Many types of organizations have implemented cashless solutions, including local authorities, government, schools and sports arenas. Such solutions typically focus on cards or wristbands containing an RFID tag, or printed with a bar code and issued to event spectators. The spectators can deposit funds into an account linked to the card or wristband, which they can then use to pay for food, beverages, commemorative T-shirts or other items. Organizations that have deployed cashless systems have realized significant benefits, including modest revenue generation, in addition to cost reductions and efficiency gains. In fact, one local authority has seen a 60 percent increase in overall efficiencies by issuing payment cards rather than paper vouchers.

The potential for generating revenue in most sectors is, as previously mentioned, modest. For U.K. football (soccer) clubs and other operators of arenas, stadia and sports events, however, the revenue increase for a scheme that is well planned and implemented can be significant. When that is added to the benefits of holding the deposited funds and having immediate access to the transactional data, the attraction for such venues is very clear.

But is this just hype, or are the financial benefits of cashless stadia truly a reality? They can be the latter, if it is a closed system that operates only within the stadium and club shop, and where the club is the custodian of the cashless scheme and the funds deposited within it. This approach vastly improves a business case based on income, and also offers the club a direct relationship with the users, as well as autonomy over the day-to-day operation of the cashless scheme, including the all-important scheme rules, particularly regarding breakage (dormant accounts with credit balances, fees for lost, stolen or damaged cards, and so forth). How users perceive the cashless scheme will be the critical success factor in terms of customer experience. In the closed scheme operated by the club, the users are truly supporting the club on many fronts—not just from the terraces and bleachers—and with the right scheme rules, the club is directly responsible for the relationship with its users.

The club could manage this type of scheme directly, or it could appoint a specialist organization to manage it while the club retains overall control. If, however, the club outsources the entire cashless process to a third party, then almost all of the financial benefits disappear, along with the direct relationship with the supporter. Although outsourcing the whole cashless process does fit with a business case built around streamlining operations to just core functions, the club gives up control over the scheme’s operation and rules to the third-party supplier. What’s more, depending on the contract terms, the sharing of transactional data may also be less than ideal. Transactional data is extremely important for providing the club with the ability to dynamically create personalized promotions and offers to its supporters via customer relationship management (CRM). If data is not available on demand, then selling those surplus XXXL team shirts will be more of a blunderbuss, rather than sniper, approach.

On the face of it, giving away so much control to a third party may not seem to be the best approach. In reality, however, what is best depends on the club’s requirements. If the club’s view is that it is in the business of playing football, and that the operational cost of a cashless solution within its stadium is a necessary evil, then outsourcing the complete scheme is exactly the right thing to do. However, if its aim is to be able to efficiently manage and nurture the relationship with its supporters, while generating additional income from intelligent but uncomplicated use of the transactional data, then outsourcing the entire cashless scheme would be madness.

The decision to go cashless either completely, or in just one section of a stadium, is not an easy one to make, and must be done only after properly analyzing the club’s overall objectives and other considerations, such as contractual arrangements with caterers and other suppliers. Then, and only then, can an informed decision be made for a best-fitting solution, and for how it should be implemented to ensure that the highest rate of customer delight and take-up is achieved.

Cashless Stadia—What Are the Benefits?

Regardless of whether the club chooses to retain control of its cashless scheme, or to outsource it to a third party, what cannot be disputed are the common benefits.

No cash handling. There will be no cash transactions within the stadium on match days, no cashing up and no more security-van collections.

Faster throughput. Because a cashless transaction can be up to 60 percent faster than cash and three times faster than credit and debit transactions, the queues at the catering kiosks move much more quickly.

Improved hygiene. The catering staff will not be handling cash—just food—thereby not only removing any related hygiene issues, but also enabling fewer employees to deliver a faster, more efficient service.

More flexible pricing. There is no reason to keep prices to the nearest dollar or pound, so this enables an item’s price to be increased by a small amount to improve revenue, or decreased slightly to boost demand.

Improved data. The transaction data via the point-of-sale (POS) terminals can tell who bought what, when and where. Such information can be utilized in personalized promotions when processed through a customer relationship management (CRM) software application.

The specific benefits of a closed scheme that the club operates either directly or via a specialist organization, and those of a fully outsourced scheme, should be carefully considered.

What to Consider When Choosing a Cashless Solution

Here are some of the important things to consider when making a decision regarding a cashless solution:

• Impact on the customer

• Effect on catering or caterers

• Legal requirements and FSA rules

• Scheme rules around breakage—poor rules around refunds, lost, stolen or expired cards can create the perception that the club, having introduced the cashless solution, is taking advantage of the fact that the user is now a captive audience)

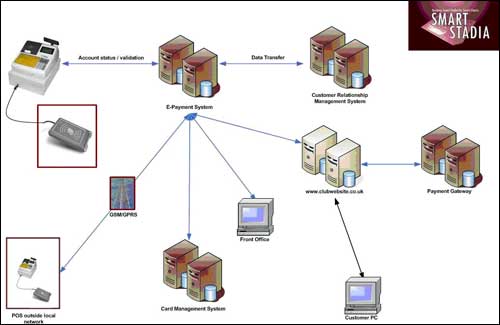

• Systems integration—the cashless system needs to be integrated with the POS and CRM systems as a minimum, as well as a card management system (CMS) for the more progressive multi-application smart card schemes

• Business model for predicting payback and forecasting revenues

Specific benefits of an in-house scheme versus one that is outsourced include:

• Transaction fees

• Financial management

• Ongoing scheme management

• Sponsorship

• Data requirements

• Customer communications and scheme promotion

• Supplier selection

• Future requirements for wider multi-application scheme

Some other points to consider:

• Which cashless technologies should be used—RFID (and, if so, which type), bar code, dual interface for backwards compatibility and so forth?

• Who will manage the data and cash flow?

Watch Out for that Banana Skin!

Technical. The danger is to get hung up on the technical details. This could be fatal for day-to-day scheme operations. Cashless solutions interfaced with a variety of other systems built with a wide range of technologies exist today in many different markets and industry sectors. While this may be new to sports stadia, it is not new for university campuses, large business premises, theme parks and many other venues. Basically, the technology works, so clubs should choose the suppliers and then let them do what they are being paid (and are well qualified) to do. That is not to say that suppliers should be given the requirements and left to get on with it, as a consistent level of effective supplier management should be applied throughout the life of the implementation.

If clubs focus too much on the technical side, this will cause them to lose sight of the back-office processes. If that happens, it will undoubtedly result in messy and expensive manual workarounds once the scheme is in operation.

|

|

Click here to view a larger version of the illustration.

Data. Another potential pitfall involves data. What will be captured, and why? What will be done with it once it is captured? What information will reside on the card, system and account? Moreover, what data does the club currently have that will enable customer accounts to be set up—and is this information clean? No matter how hard any organization may try, a percentage of the existing data will be inaccurate. The important thing is to be prepared for that contingency, and to have a good plan to avoid bad publicity, especially with regard to the deceased and those under the age of consent. No club intentionally sends an offer to someone who has been dead for some time, or an alcoholic beverage promotion to a 14-year-old—but it does happen.

Legal and Regulatory. Most important of all the potential banana skins is legislation and industry standards and regulations. In the United Kingdom, the Financial Services Authority (FSA) should be consulted for advice on any cashless solution. The FSA will almost certainly want to review the monitoring systems in place for schemes under the Small e-Money Issuer Certificate (SeMIC) rules, and this can take up to six months to achieve certificated status. The FSA’s legal language is often confusing, so consider enlisting the help of an experienced consultant with a sound understanding of the FSA regulations and a good relationship with the agency. This will help avoid delay and expense during the application process, and will prevent the risk of the scheme application failing—or, worse, allow a situation to arise that could cause the club to be liable for hefty financial penalties. Be mindful also of upcoming regulations and legal changes, such as the Payment Service Regulations of 2009 and the new e-Money Directive, slated for 2011.

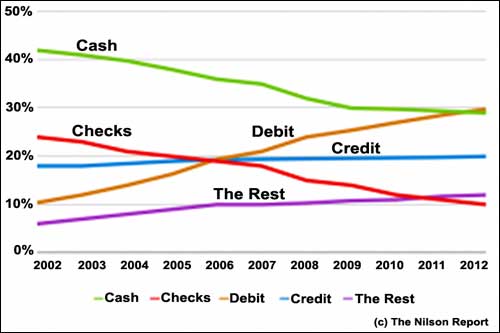

In modern-day Europe, prepaid debit cashless payment is the fastest-growing payment method, and the chart below demonstrates this.

|

|

It is important to understand that the general public is already using cashless prepaid cards as a payment method with other service providers. Mobile phone top-ups, smart utility meters, parking, vending and public transport are just a few examples.

Thus, the concept of prepaid payment is not a new one for football fans. The financial benefits to the club, as well as the improvement in the customer experience, can be very significant, not to mention the power that having the transaction data can give a club. The benefits and advantages of a carefully planned and implemented cashless solution in a football club are clear to see, and in most cases, the implementation costs could be recouped inside one or two seasons. The longer it takes to make the decision, the longer it will take to realize those benefits and advantages.

Steve Beecroft is a smart technologies consultant with Smart Stadia, a division of Consulting Smart Ltd. Beecroft founded Consulting Smart in September 2006 to meet the needs of clients within local authorities and financial services sectors. Since its launch, Consulting Smart has expanded into sports venues with Smart Stadia, and it is already working with several English Football League clubs, offering advice from concept and feasibility through to design planning, building, implementation and benefits realization.