These could hardly be worse economic times for the financial services industry. The mortgage problem snowballed last year into a global banking crisis, leading to bank failures, forced sales, government bailouts and plunges in the market cap of many of the industry’s biggest players. But while the fiscal meltdown has forced the industry to slash staff and expenses, several banking giants—including Bank of America and Wells Fargo—are actually upping their investments in RFID technology.

A number of financial institutions have started tagging and tracking assets—from laptop computers to data backup tapes—to automate inventories, improve visibility of equipment that’s checked out or moved between facilities, and prevent theft and loss. In the United States, RFID vendors say the biggest driver for the financial services industry to adopt RFID has been to ease compliance with the Sarbanes-Oxley Act, passed in 2002 to strengthen corporate governance. Another important driver in the United States, as well as in Europe, is the pressing need to better protect sensitive customer data.

|

|

“RFID automatically gives us the ability to track assets or any item that we want to have visibility into, without requiring human intervention to update databases, systems or records in our asset environments,” says Mike Russo, senior VP of automated identification technologies for Wells Fargo, which is in the midst of deploying an RFID asset-tracking system at its five primary data centers nationwide.

“Even though we use bar codes, it’s still been a manual process. To perform an inventory, you must scan each individual bar code. In a single data center, there might be 15,000 assets on just one floor. It may take a team of individuals three weeks to do that inventory by manually scanning every individual item. With RFID, I merely have to be in the vicinity—I can wheel a cart equipped with a reader and an antenna array down the aisle—without having to physically see or touch the asset. I can now do that same inventory process in a day or two.”

Leading banks early last year turned to the Financial Services Technology Consortium (FSTC), an association headquartered on Wall Street, to develop RFID standards for applications in the financial services industry so the technology would be easier for financial firms to implement. In addition to North American financial institutions, members of the FSTC include technology vendors, independent research organizations and government agencies.

In December, the FSTC released its first RFID standards, detailing the types of RFID tags that should be employed and where they should be placed on IT assets. The group determined that for IT asset management, the tags should be EPC Gen 2-compliant and should be attached to the front face of rack-mounted assets, including servers, blade chassis, blade servers, network switches and peripherals, such as backup tape drives. It also called on computer and equipment manufacturers to start RFID-tagging hardware during manufacturing to enable automated shipping and receiving.

The development of standards is seen as a positive sign to encourage RFID adoption in an industry that is undergoing a change of epic proportions, with many hastily arranged mergers and acquisitions and a general fight for survival. “What the industry has learned over time is that when you merge and acquire other organizations, the biggest opportunity you have in doing these things right is how you blend your information together,” says John Fricke, FSTC chief of staff. An asset-management system might differ from bank to bank, so after a merger, it’s imperative to combine the two systems into one for the newly merged organization. “If you have a standards process, everyone is playing with the same standards and same rules,” Fricke says. “It will go together a lot easier, a lot quicker and cost a lot less.”

Given the potential savings from asset tracking, financial institutions are now exploring other ways RFID could help their organizations improve business practices, such as creating a paper trail of documents and even keeping tabs on money. Some banks are employing RFID to provide customers with more personalized services.

Improving Compliance and Accounting

Provisions of the Sarbanes-Oxley Act require proper accounting of fixed assets, such as computers and other equipment in data centers. Sarbanes-Oxley has put tremendous pressure on global banks to understand where their assets are, whether there are ghost assets (those they don’t have anymore) on their books, and what they need to write off in terms of lost or misplaced products. The federal law also requires companies to document how they gather information on assets—meaning many of them need to establish some type of auditable paper trail.

|

|

The data collected with RFID can provide that accounting and paper trail. “Under Sarbanes-Oxley, you need to know where all your stuff is, especially expensive stuff like computers,” says John Rommel, senior manager of RFID channel development for Motorola, which serves on the FSTC RFID committee. “All these assets are being depreciated on their books, and companies have to answer the question, ‘Do we still have them?’ ”

Compliance with Sarbanes-Oxley was one reason Bank of America, in the past year, deployed RFID at 14 of its 38 data centers for tracking computer servers and other high-value IT assets. Within Bank of America’s data centers, mobile RFID interrogators are mounted on carts that employees wheel up and down rows of server racks to automatically read the tags attached to assets. In addition, portal readers mounted around the doorways collect information from tags as assets are removed from—and returned to—the data centers.

The project had three main goals, according to William Conroy, head of Bank of America’s enterprise architecture division, speaking to attendees at the EPC Connection 2008 conference in October. The first was to realize time savings when conducting inventories. The second was to have up-to-date and more accurate inventory data to simplify compliance with Sarbanes-Oxley and other regulations requiring companies to account for corporate assets. And the third was to limit risks associated with protecting customer data—a business imperative in the banking industry.

Protecting Customer Data

Financial institutions accumulate tons of sensitive customer data—from bank account deposits and withdrawals to credit card transactions. The data is maintained on computers, hard drives and backup tapes for years. Banks often need to transport this data to credit-rating groups and federal regulators, as well as between their own facilities. Ameritrade, Bank of America and Citibank are among the financial institutions that, during the past few years, have had to notify their customers that their personal data may have been compromised by the loss or theft of IT equipment.

In August, the revelations hit a new low. The United Kingdom’s Information Commissioner launched a probe into how a secondhand computer containing personal data on a million customers—of businesses such as American Express, NatWest and the Royal Bank of Scotland—was sold in an auction on eBay for £35, according to Britain’s Daily Mail. The computer had belonged to an outside company called Graphic Data, which stores information for financial institutions.

To better protect data, financial institutions and some of the data warehouses that act as repositories for their data are deploying and experimenting with RFID to ensure that computers, data tapes and hard drives don’t leave facilities without proper authorization. “The single most important product they sell is trust,” says Daniel Connolly, head of worldwide sales for Odin Technologies, an RFID integrator that has been active in the FSTC standards-making process. “It’s the trust their customers have in them, knowing that they will be able to protect financial data and the integrity and sensitivity of the data.”

In 2007, Wells Fargo installed an RFID system to track laptop computers as employees leave the company’s Roseville, Calif., data center. The system replaced a manual check of computer bags by security guards at the building’s exits, which created long lines. Attached to each computer is an ultrahigh-frequency passive Gen 2 tag with a unique ID number. That number is linked in Wells Fargo’s databases with the computer serial number, as well as with the name and photo of its authorized user. As an employee leaves the building, an RFID interrogator captures the ID number, and the person’s name and photograph appear on a monitor at the guard station.

In addition to the asset-tracking program at five of its data centers, which involves tagging servers, hard drives and other computer assets, Wells Fargo is in the process of implementing an RFID project to track data backup tapes in its data centers. The tapes will be tracked throughout their lifetime—as they are checked out of libraries, moved between facilities and archived in secure storage. “We’re going to be tagging every tape,” Russo says. “We want to ensure that visibility and having the augmented audit trail is an added layer that enhances our ability to know where any tape is at any point in time.”

In 2008, Bank of America started tracking data tapes as they are checked into and out of data center facilities. At the EPC Connection conference, Conroy said the bank was considering upgrading the system to trigger an alarm when a portal reader detects a magnetic tape being removed from a data center before it is properly cleared for removal.

|

|

In the future, RFID may be used in conjunction with GPS technology to give financial institutions the ability to track the location of tapes as they are moved between facilities and to storage vendors. “People want to be able to not only locate the tapes more quickly and track the tapes between locations, but they envision taking a cartridge and maybe associating it with a carrying case with a GPS tracker inside,” says Nancy Kingston, global sensor solutions executive with IBM.

Another source of concern for financial institutions is the assortment of hard drives on which sensitive information is stored in data centers. These hard drives are continually being upgraded and/or replaced as the technology yields faster speeds and increased storage capacity. Financial institutions want to ensure that the old hard drives are erased and destroyed to prevent the extraction of any sensitive data. “We track all hard drives with RFID throughout their life cycle,” says Wells Fargo’s Russo. “We have a complete audit trail of that hard drive—from server, to local storage and destruction, to recycling.”

Some banks rely on outside data warehousing companies to secure their backup data on hard drives or tapes. Alien Technology is currently working with a data warehousing company that serves the financial services industry to develop a pilot that uses RFID to track hard drives from their use in the data center through to their eventual destruction. “They want to make sure it doesn’t get put down on a desk and forgotten,” says Scot Stelter, Alien’s director of reader product marketing. “One of their main motivations is to establish a certified paper trail.”

Tracking Documents and Money

Despite the rise of electronic banking and monetary transfers, banking is still a very paper-intensive business. Loan documents, certificates of deposit and even cash are moved from office to office, from branch to branch, and sometimes from one institution to another or to government agencies. “It’s still a paper economy at the core,” says Odin’s Connolly. “It requires that paper element to protect the integrity of transactions taking place, the need to have the physical asset of a title or loan agreement to validate that the exchange did take place.”

Several financial institutions worldwide are employing or testing RFID to create a paper trail—tagging documents, or folders, totes or cases that contain documents, and tying that information to a unique number in a searchable database so the documents can be located quickly. Austria’s Hypo Landesbank Vorarlberg has been using an RFID system since 2003 to track paper files on each loan it makes to customers. Tens of thousands of tagged files are now either in circulation or stored at the bank’s headquarters in Bregenz. “We have not had one file misplaced,” says Peter Steffani, who works in the bank’s IT department.

In Asia, several financial and legal document storage companies have been deploying RFID to keep track of files so they can be easily located and recalled if needed, according to Jarrod Sinclair, an RFID consultant at HP who deals mostly with financial services customers, including document storage companies. Sinclair says that sometimes the documents are loaded into pre-tagged envelopes or boxes, and other times the documents are tagged as they arrive at facilities so they can be inventoried automatically.

In addition to tracking documents with RFID, a growing number of financial institutions are investigating whether the technology can be used to track bags of paper assets—from cash to checks and certificates of deposit—that are routinely transported, to ensure that monetary assets are delivered to the right customer, facility or branch. These bags are now tracked using mostly manual methods, such as checking off lists of serial numbers on a sheet of paper or scanning bar codes. RFID could automate the tracking so that shipment and receipt are recorded when the bags are delivered to a dock door or branch office. FSTC members have asked the consortium to develop standards for tracking documents and bags, which will make the technology easier to deploy and enable transfers among different companies.

Odin’s Connolly says that smart container technology could be used to secure cash bags, and would even provide a mobile element if deployed in armored trucks or other delivery vehicles. “You could have a portable RFID reader and antennas that mount on the inside of a truck or a van,” he says. “Once installed and powered up, they could interrogate everything inside the truck.”

The automation of business processes is another goal of the FSTC, which has been encouraging manufacturers of computers, hard drives and backup media to start RFID-tagging equipment during manufacture. “The quicker we get a standard that we all agree with and get the vendors to pre-tag the equipment before it arrives, the quicker we can also get the vendors to send notifications to the buyer in advance, including what the tag number is, so that they can update their asset-management system,” says the FSTC’s Fricke. “When it arrives at the loading dock, they’ll know it’s here, and they can track the whole process.”

|

|

While the economic crisis has certainly put a dent in IT budgets for financial services companies, RFID is one investment that is expected to pay off over time. One large company that deployed an RFID system found computer equipment it didn’t know it had, thereby making up for the cost of the RFID deployment, Fricke says. Some financial companies are retrofitting their data centers with RFID tags, but others hope to more gradually RFID-enable their processes with pre-tagged equipment. “Most organizations turn the hardware in their data centers over every two to three or every three to four years,” Fricke says. “If you started this process now and let it go over a normal course, in five years everything in the data center could be tagged.”

Some vendors have already stepped up to the plate. As a service to banks and other customers, HP will RFID-tag computer equipment before shipment. IBM announced in October that customers could order select backup tape cartridges with pre-affixed RFID tags.

In the hotly competitive financial services market, global giants see value in sharing what they learn from RFID through the standards-making process at the FSTC. “If we’re all going to do this as independent entities, we’re going to discover the same problems and pitfalls,” says Wells Fargo’s Russo. “It’s much more effective when we can co-develop some of the solutions for tag and reader analysis, tag placement, encoding schemes and labeling standards. We’re not giving away company secrets by working together to help the industry ID best practices that we can all leverage.”

Meet, Greet and Sell

Yes Bank, a commercial bank with 101 branches across India, has been testing an RFID system at its suburban Delhi branch for six months that enables employees to identify and greet customers as they walk through the door. The technology, provided by SkandSoft Technologies, has proved to be popular with customers who have high expectations for personalized services, so now Yes Bank plans to roll out the RFID system in several other branches. (The deployment was set to begin in early December, but was postponed due to the terrorist attack. At press time, it was scheduled to start in January.)

For the past few years, Accenture has operated a “bank of the future” branch in France where RFID helps employees welcome customers and provides account managers with the opportunity to sell them additional products and services. While banks like the idea of employing RFID to improve customer services, concerns about privacy have prevented many from buying into the “meet-and-greet” solutions. But some banks are in investing in the “sell” applications.

|

|

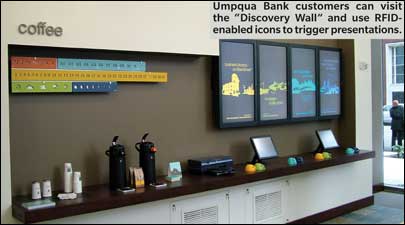

Two years ago, Umpqua Bank, a U.S. bank with 200 locations, started using an RFID application in branches around Portland, Ore., that allows customers to access digital brochures about bank products, such as home loans or business banking. In an interactive area called the “Discovery Wall,” which features ultrahigh-definition video screens, consumers can pick up RFID-enabled 3-D icons that sit on a shelf on the wall. Each icon represents a different bank product line and triggers an interactive presentation on a touch screen. After interacting with the digital brochure, a customer can print the document.

“Financial services companies have a need to communicate more directly to their clientele,” says Bryan Fairfield, VP of sales for Nanonation, which made the software for Umpqua Bank‘s RFID application. “And the customers who spend their money in those establishments want more direct communication of information that’s valuable to them.”

This type of marketing is more effective than advertisements, Fairfield says. “There is a specific time and place where that customer expects that communication,” he says. “RFID allows you to raise that to a new level of targeted marketing.”