In La Junta, Colo., local consumers have begun to refer to their payment transactions as “Blinging.” The term comes from a new contactless payment application provided by California payments network startup Bling Nation, in conjunction with The State Bank and Viaero Wireless, a provider of cell-phone service to rural communities in Colorado and Nebraska. The application enables a consumer to employ an adhesive RFID label attached to his or her mobile phone, to pay for local purchases at approximately 60 area merchants. The transaction cost is deducted from the customer’s bank account, and a receipt and account balance update are sent as a text message to the individual’s phone, all in a matter of seconds.

The system has been in place since early June 2009. To date, about 35 percent of The State Bank’s La Junta clients have begun using the Bling/State Bank sticker, which contains a passive 13.56 MHz RFID tag compliant with Near-Field Communication (NFC) standards, to pay for purchases, while approximately 90 percent of local retailers have signed on with Bling payment devices installed at the point of sale (POS). Three other communities in California and Colorado will soon be Blinging, with merchants at two of the sites already installing the POS devices.

Wences Casares and Meyer Malka, co-CEOs of Bling Nation, launched their company to develop a contactless payment solution after previously establishing Banco Lemon, a Brazilian firm that has since been acquired by Banco do Brasil. Banco Lemon provided bank accounts to low-income individuals who previously lacked bank accounts. The bank accepted cash deposits from its customers, providing a receipt with a bar-coded ID number. An account owner could then take the bar-coded receipt to participating stores, where it would be scanned, enabling that person to either withdraw cash or pay for purchases. As a result of the bar-code-based system’s popularity in Brazil, Casares explains, he and Malka decided to launch a U.S. company with a contactless system that would result in low transaction fees for merchants, and also be convenient for customers.

Casares notes that traditional debit or credit card purchases require that merchants pay a transaction fee, in large part because of the multiple players involved in each transaction throughout various parts of the world. Those players often include the local bank, a global financial services provider, such as MasterCard or Visa, and a communications service provider to move data throughout multiple databases.

However, Casares says, a large percentage of non-cash payment transactionsare accomplished locally, just miles from a cardholder’s issuing bank, particularly in small towns. So Bling Nation began seeking a lower-cost option for regional banks that would be more direct than debit or credit card payments, and would thus reduce the merchants’ transaction fee compared with what they pay for purchases made using a debit or credit card. By bringing Viaero Wireless into the equation, the company could send information via a cellular connection to and from the bank’s and Bling’s servers, as well as transaction receipts to customers over their cell phones. And NFC technology would make the actual payment function faster, sparing customers from ever taking out their wallets, searching for cash, signing their names or inputting passwords.

This summer, customers received a BlingTag—a quarter-size NFC sticker adorned with The State Bank’s and Bling Nation’s logos—in the mail, along with their bank statements and instructions for activating the tag on the bank’s Web site. Users then affixed the adhesive tags to their phones. Each tag has a unique ID number that, once the system is set up, links to the phone owner’s State Bank account.

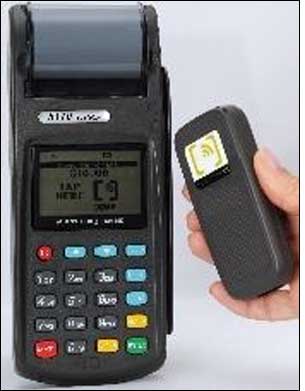

Upon making a purchase, a customer taps the phone near the merchant’s BlingTag NFC reader, which captures the tag’s ID number. A Viaero Wireless SIM card in the BlingTag interrogator transmits that ID number over the cellular network to The State Bank, where Bling software links the ID number to the account. The bank can verify the balance, ensuring there are sufficient funds to pay for the transaction, then deduct the payment amount from the account and send an “approved” signal to the Bling reader. At the same time, the interrogator encodes the BlingTag with a new, randomly generated ID number and deletes the old ID number, thereby providing greater security in the event that someone acquires the tag’s stored ID number during a transaction and attempts to reuse it.

For those transactions deemed high-risk, such as purchases over $75, an automated call is made to the customer’s phone, requesting a password entry using the phone keypad. If the system cannot contact the customer via phone, the BlingTag Reader will instruct the user to enter his or her PIN on the keypad at the payment location.

The customer then receives a text message on his phone from Bling Nation, indicating the purchase amount, and also listing the remaining balance in his bank account.

Bling Nation charges participating merchants a fee for each transaction, but Casares indicates that it is about half of the cost they pay for debit card transactions, and an even smaller percentage compared with credit card transactions. That fee varies, according to the type and size of the business.

Although the system was initially designed as a low-cost alternative for merchants, Casares says, to the debit and credit card transactions, the other benefits associated with the system have made it desirable as well. “We’ve learned that this makes a lot of sense to merchants, not just as a cost advantage,” he states. For instance, stores also utilize the system to provide customers with loyalty points. In this case, Bling Nation stores customer data, such as the number of purchases that person makes at a business, and issues a reward when the patron’s purchases reach a predetermined quantity—for example, the customer might earn a free cup of coffee after making five purchases at a coffee house.

The system has been popular among bank customers, Casares says, noting that someone in town recently commented to him, “I’ve even got my grandmother Blinging.” The convenience of the NFC technology, he indicates, makes a transaction possible in approximately five seconds. “After they’ve used it for awhile, they say a traditional credit or debit card feels counterintuitive.”

The Bling system works best in small communities, Casares says. The company chose La Junta to launch the system, he notes, since it has only about 8,000 residents, most of whom make purchases in the immediate area. The firm now plans to expand to communities with a population of 30,000 to 100,000, and hopes to sign up another 10 banks by the end of 2009. Within two years, he adds, Bling hopes to begin exploring suburban areas to deploy the system. The company is also in discussions with several universities to pilot the technology for students using Bling Nation’s services on their student ID cards.