Aug 01, 2006Citigroup, the nation's largest financial services company, reported in June 2005 that backup data tapes containing personal information on 3.9 million customers were lost by UPS during transport to a credit bureau. Citigroup—like ABN Amro, Bank of America and Peoples Bank, which also lost backup tapes last year containing personal information on millions of customers—had to notify its customers of the potential privacy breach under a series of new state laws. Analysts estimate it costs companies up to $1 per notification letter, but the loss of data tapes also can tarnish a bank's brand and put customers at risk of identity theft.

It became clear to the financial services community that a better system was needed to keep track of these valuable computer tapes. A few of the world's largest banks are currently involved in pilots or discussions to see whether RFID can help them safeguard the tapes. The financial services industry is similar to other businesses adopting RFID—such as retail, aerospace and pharmaceuticals—in that it is interested in tracking shipments of physical goods. In addition to backup tapes, financial institutions are testing the use of RFID to secure shipments of currency, bearer bonds, gold and checks from loss or theft.

|

|

Banks and credit card issuers are already using RFID technology to offer contactless credit cards or prepaid debit cards, which can speed payments at convenience stores and gas stations. In the past year or so, American Express, Chase, MasterCard and Visa, among others, have rolled out contactless payment systems in select markets around the world (see "The Cashless Reality," July/August 2005).

Now banks are exploring whether RFID can help to personalize customer service. Insurance companies also are exploring future uses of RFID. They would like to replace estimates with real data that can help them more accurately manage risk, underwrite policies and pay out claims.

Securing the Data Trail

Banks amass hundreds of thousands of data tapes, which record a range of information from bank accounts to credit card transactions and loan applications. Most tapes are now tracked with bar codes and can be located and retrieved using those numbers from automated libraries at bank data centers. But banks often need to transport this sensitive client and transaction data to credit-rating groups and federal regulators, as well as between their own facilities. It has been during the transportation process that most tapes have been lost. Tapes also have been misplaced after employees checked them out from bank libraries to verify data.

After the high-profile loss of data tapes, some banks immediately sought to switch to electronic transfers of encrypted data. Other banks turned to a combination of GPS to pinpoint the location of trucks carrying data tapes and RFID to tamper-proof the cases that hold the data tapes. Several other banks are piloting or discussing the use of RFID to tag every data tape cartridge to know who removes the tapes and when, and to track the tapes to their destination.

To track the tapes in the Unisys pilot (the company won't identify the bank), thin labels embedded with passive RFID tags were attached to every tape cartridge in the data center. Interrogators were set up at the door of the center to record when tapes, stored in plastic tubs, are removed. Employees of the bank or logistics company transporting the tapes are issued RFID-enabled identification cards to ensure that they have authorization to remove the tapes. The tubs have been fitted with an active RFID electronic seal combined with cellular technology, to provide both location tracking and verification that the tub has not been opened.

|

|

"If you put 15 tubs on a truck together and one tub starts moving away from the others, it alerts you," Regen says. "If it falls off the truck or is moved from the vicinity of the others or left behind, it can scream for help and tell you where it is."

Another top-10 U.S. bank is tracking data tapes using a combination of passive and active RFID technology from Axcess International, and data center services and products from Media Recovery. Jim Ferguson, Axcess vice president of strategic sales, says the company has designed a passive RFID label for the side of the data cartridges, and two active tags—one integrated into the carrying case, which holds about 20 data cartridges, and the other used on the employee identification badge to provide access to the data center to remove tapes. Participants report success.

"It's almost 100 percent in testing now that nothing gets out without being recorded," says Debbie Hicks, marketing director for Media Recovery.

Eagle Global Logistics has a banking customer that is using a combination of RFID and GPS to track data tapes in transit. The technology solution from Argo Tracker, an asset-tracking company, alerts bank officials if a case has been opened en route, and allows them to know if the cases that hold data tapes are being loaded or unloaded in the proper time frame. Cargo trucks are fitted with a combination GPS device and RFID interrogator, which takes continuous readings of RFID tags and sensors put on cases. The information is transmitted in real time through a wireless network back to the bank's security officials. "We've set it up so that an alarm is triggered every time a security sensor is triggered on one of the cases," says Mike Hammons, CEO of Argo Tracker.

In 2003, there was a rash of news reports in trade magazines in the United States and Europe that the European Central Bank had undertaken a "hush-hush" project to embed RFID tags into the very fibers of euro bank notes. The reports said the project was designed to foil counterfeiting of the currency as countries in the European Union prepared for the changeover to the euro. The project was never implemented, according to Niels Bunemann, a spokesman for the European Central Bank, in Frankfurt, Germany. But Bunemann would not comment about whether such research was ongoing. "On research projects on the future security features of bank notes," he says, "I can neither confirm nor deny that we are, in fact, looking at this or planning for this."

While industry consultants say that integrating the RFID tag and antenna into paper currency is technically possible, the high cost of chips makes it unclear whether the benefits would justify the cost. Bank notes are already protected from counterfeiting by such features as holograms, foil stripes, and special inks and watermarks.

|

|

But the idea of using RFID to track bags or bundles of currency, bullion and even canceled checks has taken off in other areas. Regen says Unisys has conducted proof-of-concept pilots for a government institution involving the tracking of physical money within a large facility. He wouldn't disclose the government or the agency because of security concerns. But Unisys is currently helping the U.S. Department of Defense track shipments of cash and other valuable goods with RFID.

Some European firms also are in the early stages of testing the feasibility of using RFID to track bags of cash, security documents, bearer bonds and other valuables. "Banks want to be able to track where such packages are," says Mark Greene, vice president of strategy for IBM's Financial Services division. Due to security concerns, he declined to name the firms.

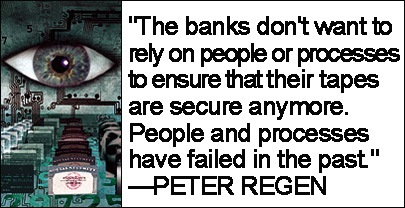

Whether financial service institutions are tracking data tapes, currency, bearer bonds, diamonds or other assets, most are likely to take their time testing the technology before making the investment to deploy RFID. Financial service firms are interested in RFID to help protect "brand, reputation, security and the cost avoidance of an incident," says Regen. At the same time, "these are organizations that want to be very sure that this will work before they make the investment to do this full scale."

A department store warehouse that uses RFID to track every pallet of each type of product stored would have a precise, up-to-date accounting of insured goods. This record could be used in case of a fire or some other catastrophic event to file an insurance claim. Insurance companies also could use such real-time data to set rates, pay out claims and manage risk.

At the year-old Technology Innovation Lab in Hartford, Conn., The Hartford Financial Services Group, one of the largest insurers for individuals and businesses in the United States, is analyzing how RFID, sensors and other emerging technologies might impact the insurance industry. "There is a level of granularity that RFID could provide us across those areas of pricing and loss control and claims processing that is very appealing to us," says John Anthony, director of the lab. "That's why we're spending the time and energy to understand the capability of the technologies and how our customers are using those technologies."

Using RFID to track railcars or truckloads of goods, for example, might help a retailer cut down on losses due to theft or misplacement, and that could be reflected in lower rates. In the same respect, ensuring that shipments of produce are kept at optimal temperatures during transit by using sensors in conjunction with RFID could result in less spoilage and fewer claims.

Insurance is an industry that is all about managing risk. RFID could help companies lower overall risk by providing real-time information about location and perhaps condition of assets, as well as real data about the transfer of assets from one party to another—for example, from manufacturers to retailers.

The lab is working in conjunction with The Hartford's underwriting, loss control and claims businesses to understand how access to information from RFID and other technology could help the company offer new products and services to customers. "Hypothetically speaking, we may have set up a worker's compensation policy dependent upon certain situations existing and certain situations not existing, such as workers not entering into a certain part of the factory floor when they shouldn't be there," Anthony says. Using RFID to track employees, that factory could gain a more realistic picture of the extent to which its workers are visiting a dangerous area, perhaps reducing future injuries and claims.

Insurance also is a data-driven industry, which makes it a natural fit with RFID. "Ultimately," Anthony says, "the use of RFID to price insurance policies and help in claims management is largely dependent on the extent to which our customers adopt RFID."

RFID-enabled ATM, debit and credit cards may one day allow bank managers to provide more personal service to their customers. As customers enter the bank, RFID interrogators in the doorway would read their cards' RFID tags, identifying them to bank personnel, who would greet them by name, direct VIPs to sales associates without making them wait in line, or instruct tellers to pull up customer records in advance.

Those are some of the scenarios being tested by a handful of banks in Europe and North America that could transform services at the branch level. Consultants say using RFID to save customers time and provide personal assistance could help banks foster customer loyalty and increase their share of a customer's business. That's a growing goal in a market that tends to be fragmented, with customers often having savings in one bank, credit cards with another and their mortgage with yet another bank.

One large retail bank in Europe conducted a pilot program last year with Unisys, testing the use of passive RFID bank cards on focus groups and employees. The bank selected one branch and installed interrogators at a number of strategic locations, including at the entryway, in the line for tellers, and at a promotional display for auto loans and mortgages. The test found that a bank could use the data gathered to provide premium customers with higher levels of service, such as personal greetings, shorter waits in line, portfolio reviews and personalized care from sales associates.

Accenture has established a "next-generation branch" in Sophia Antipolis, France, to showcase how RFID and other technology applications could simplify and differentiate bank services. Accenture was exploring a pilot with a North American financial institution late last year for using RFID cards to provide a differentiated level of service to its VIPs, and has had discussions with many other interested financial institutions around the world. "Everybody is doing this in secrecy right now," says Christopher Pacourek, the financial services innovation lead at Accenture Technology Labs. "They don't want to say, 'Hey, we're going to launch this VIP service.'"

IBM is involved in pilot programs with three banks in the United States and Europe that use RFID-enabled bank cards for in-branch programs designed to increase customer loyalty. The banks are interested in bettering services for wealthy individuals and other premium customers. Some of the pilots have been going on for a few years, says Mark Greene, vice president of strategy for IBM's financial services division, but there are no plans for wider-scale implementation, because the banks are concerned about ensuring customer privacy.

It's also possible for banks to use RFID data to determine accurate bank traffic at certain times of day. "If you know that the average person who comes into a branch spends 25 minutes, including spending 14 minutes waiting in line, you can better design the branch and staffing to meet customer needs," says Peter Regen, vice president of Unisys' global visible commerce division.

So far, none of the RFID pilots has been turned into a full-scale deployment, because banks are concerned that customers may be apprehensive about participating due to privacy concerns. But consultants say banks could be deploying RFID technologies within five years or less if they convince VIP customers that there are premium services to be had in exchange for a bank's ability to know when they walk into a branch. The trade-off would be similar to a customer's decision to use a supermarket loyalty card, allowing the store to gather data about their purchases in exchange for discounts.

RFID cards would be offered to customers on an "opt-in" basis. And customers who opt in could be issued foil-lined slips into which they could insert the RFID card if they did not want their movements tracked inside a branch, Regen says. The foil would block interrogators from receiving signals from the card's RFID chip.

Another obstacle is the technology itself. Unisys conducted pilot programs with passive RFID tags embedded in existing bank cards, so the same card could be used at an ATM or swiped through a debit card reader. But the RFID readings inside a bank branch were inconsistent when the cards were kept in a wallet or a pocket close to a person's body, as opposed to a purse, because the high amount of water in a body interferes with the transmission of passive RFID signals. Accenture says banks need to use active (battery-operated) tags in cards for in-branch applications. But the technology hasn't evolved to the point where a chip and battery could be fitted into a format as flat as a bank card. Vendors say that will soon be possible, but the cost of such cards would be roughly $10 each, compared with 40 cents for a magnetic-stripe card—a bit too pricey for banks to get more personal with their customers.

Illustration by Michael Morgenstern.