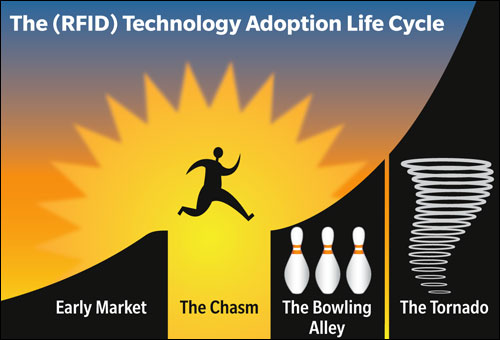

Apr 01, 2010In his bestseller Inside the Tornado, Geoffrey Moore explains that new information technologies pass through several distinct stages before they enjoy widespread adoption. In the first stage, which he calls the Early Market, "technology enthusiasts" who hear that a new technology can deliver a clear and compelling benefit over existing technologies work with vendors (usually startups) to develop solutions that fit their needs. Visionaries take these basic solutions and adopt them to try to gain a competitive edge.

In the second stage, called the Chasm, vendors offer these solutions to other end users, but the technology meets with resistance because the solution isn't complete enough to satisfy all their needs. Moore says there's a chasm between the visionaries and "pragmatists"—those who will invest in a technology only when everyone else invests in it.

In the third stage, technology companies build a "whole product" that meets the needs of a market segment. Pragmatists in that niche who have specific business problems that the technology can solve begin adopting it. At this point, the technology has crossed the chasm and is now in what Moore calls the Bowling Alley. Technology providers try to achieve widespread adoption in that niche, so they can knock over a bowling pin (one market segment). When they've knocked over one pin, they try to adapt their product and sell it to another segment and then another.

In the fourth stage, one vendor emerges as the market leader. With a clear choice, pragmatists move as a herd to adopt the solution. Companies that previously didn't need the technology now must have it—and the technology enters a period of rapid growth. Moore calls this the Tornado.

So based on Moore's model, which has proved correct for many technologies, which stage of the RFID adoption life cycle have various industries reached? Most are in stage three, where vendors are building a whole product and pragmatists are starting to adopt it to solve business problems. The number of companies in specific segments will continue to increase, and vendors will continue to develop products that are more complete. Many early adopters report that they are gaining a competitive advantage over companies sitting on the RFID sidelines.

For pragmatists to adopt the technology en masse, there must be agreement on a technology standard, a whole product that meets the industry's needs and a market leader. Different industries are closer to widespread adoption than others.

Apparel retail: Studies conducted by the University of Arkansas' RFID Research Center have shown that RFID offers a clear benefit over bar codes, for both retailers and manufacturers. And a handful of visionary companies—such as American Apparel in the United States, Charles Vögele in Switzerland and Throttleman in Portugal—have proved RFID can be used to better manage store inventories.

The apparel industry seems to have agreed on passive UHF (ISO 18000-6C) as the standard. Technology companies have been working in partnership to provide the whole product in the marketplace. Motorola has provided handheld and fixed readers for a number of deployments. Avery Dennison has supplied RFID-enabled hangtags, which usually have Impinj RFID chips in the transponders. And OATSystems, Xterprise and ADT's Vue Technology have developed the software solutions for apparel retailers.

Europe has clearly crossed the chasm; expect to see more apparel retailers adopting RFID. The U.S. apparel retail sector is slightly behind Europe, but there will be more pilots this year. As the success of these deployments gets publicized, more apparel retailers will begin to consider adopting the technology. It will likely be at least another year or two before a clear market leader on the software side emerges to propel adoption, but this sector is close.

Consumer packaged goods: The use of passive UHF systems was originally driven by the CPG industry. Gillette and Procter & Gamble were the founding members of the Auto-ID Center (before they merged), which promoted the use of low-cost RFID tags carrying Electronic Product Codes. Retailers, including Wal-Mart and Target, soon joined. Target saw no return on investment and did not deploy an RFID solution. Wal-Mart saw some benefits, but there was no clear and compelling benefit to its CPG suppliers. Wal-Mart shifted its focus to look for other areas where it could benefit from using RFID. As the cost of RFID tags and readers comes down, CPG companies may find benefits. But for now, they're stuck on the wrong side of the chasm.

Defense: With the U.S. Department of Defense (DOD) pushing suppliers to use passive UHF tags on cases and pallets, there's a prime mover that could encourage adoption of RFID in the defense industry. But the DOD is using a variety of software solutions for passive tagging, and it's not clear the technology will create much business value for suppliers. More suppliers might tag for the DOD, but widespread use of passive RFID within the defense sector seems to be a few years away, despite the DOD tagging requirements.

Some have predicted that health care will be among the first industries to "enter the tornado"—that period of rapid mass technology adoption. But that seems unlikely within the next 24 months, because there's no standard for using RFID to track assets. Some hospitals are using ZigBee-based solutions, others Wi-Fi and still others proprietary active RFID systems. Most hospitals will wait to see which type of system and which vendor emerge as the clear leader before adopting.

Logistics: The global logistics industry, with a few exceptions, has been relatively slow to embrace RFID. But the DOD's use of active RFID technology based on the ISO 18000-7 standard could propel adoption of active RFID in the logistics industry. That's because the DOD is helping to build out the tracking infrastructure at ports and using active RFID tags (based on the ISO 18000-7 standard) on containers shipped on commercial vessels. Savi Technology has a clear lead in providing both the hardware and software to the DOD. More ports are also using the ISO-standard tags to track containers and vehicles. If Savi can convince logistics companies there's a clear and compelling benefit for them (as well as for the DOD and the ports) to RFID-tag containers and use its software to track those containers, Savi could emerge as the market leader around which pragmatists in the logistics sector could rally.

Manufacturing: RFID has delivered a wide variety of benefits to manufacturers, including the ability to track returnable containers, parts bins, tools and work in process. The clear and compelling benefits have been largely around using active RFID and RTLSs in large manufacturing facilities. There are many companies that offer solutions for locating assets, but it doesn't appear that any one company—or even a group of companies working together—has a clear lead. It's likely that solutions will continue to evolve for several years before a market leader emerges.

Pharmaceuticals: Most pharmaceutical companies scaled back their RFID efforts when states delayed their requirements to collect individual pedigrees on each dose of drugs until at least 2015. Some companies, such as McKesson, are examining the internal benefits they can achieve from tagging reusable totes, but there's currently no clear and compelling benefit to adopting passive UHF systems on individual doses. If more states adopt pedigree laws, RFID will provide big benefits over two-dimensional bar codes, which necessitate high labor costs to capture data. Adoption could be propelled not by the market Moore describes, but by government regulation.

Retail: Mass-merchandise retailers (Metro and Wal-Mart) and department stores (Bloomingdale's and Macy's in the United States, and Galeria Kaufhof in Germany) have been tracking goods with passive UHF tags based on the ISO 18000-6C standard. Both categories see benefit in tagging apparel. But tagging slower-moving items, such as furniture and appliances in department stores, and soup cans and cereal boxes in mass-merchandise retail, delivers less benefit. It's likely these retailers will focus on specific categories of goods, such as jewelry, high-value electronics and DVDs. Several companies make solutions that can be used to track inventory in mass merchandise retail and department stores, but solutions specifically designed for these sectors are still emerging. Mass-merchandise retailers and department stores will likely follow apparel retailers in the adoption cycle.